As local, state, federal government, and supranational agencies are racing against time to reduce greenhouse gases, ammonia is gaining attention as a “green” fuel for decarbonizing the transportation sector. But so far, much of that attention on ammonia’s applications has been limited to the marine transportation sub-sector.

Ammonia (NH3) is produced by combining gaseous hydrogen with nitrogen from the air. Large-scale ammonia production uses natural gas for the source of hydrogen (grey hydrogen). However, if the market for clean hydrogen takes off, ammonia can be produced cleanly as well.

To be clear, ammonia fueled engines and vehicles are not new. During World War II, Ammonia (liquid anhydrous ammonia) was used to power buses in Belgium. Around the same time, the Gazamo process (burning a mix of ammonia and hydrogen in internal combustion engine) appeared to be the first application on a large-ish scale, with about 100 vehicles equipped for use of ammonia as fuel.

In the 1960s, the U.S. Military funded the Energy Depot Project, which explored developing alternative fuels (hydrogen, ammonia, and hydrazine) from indigenous materials (water, air, earth) but concluded that as long as hydrocarbons (e.g., gasoline, diesel, kerosene) are available, there was no incentive to use alternative fuels.

Recently, Toyota unveiled a 2-liter, 161 horsepower ammonia powered engine. Built in collaboration with Chinese automaker GAC Motor, the engine is touted to be a revolutionary breakthrough that will end EVs. To make the ammonia engine clean enough to use, Toyota and GAC had to cut nitrogen emissions, which was achieved in part due to an increase in combustion pressure.

There is also something in the works for heavy-duty trucking. Amogy, a cleantech startup that specifically aims to use ammonia to enable the decarbonization of the hard-to-abate sectors, unveiled the world’s first ammonia-powered semi-truck in early 2023. The 300kW semi-truck has 900 kWh of total stored net electric energy and can be refueled in 8 minutes.

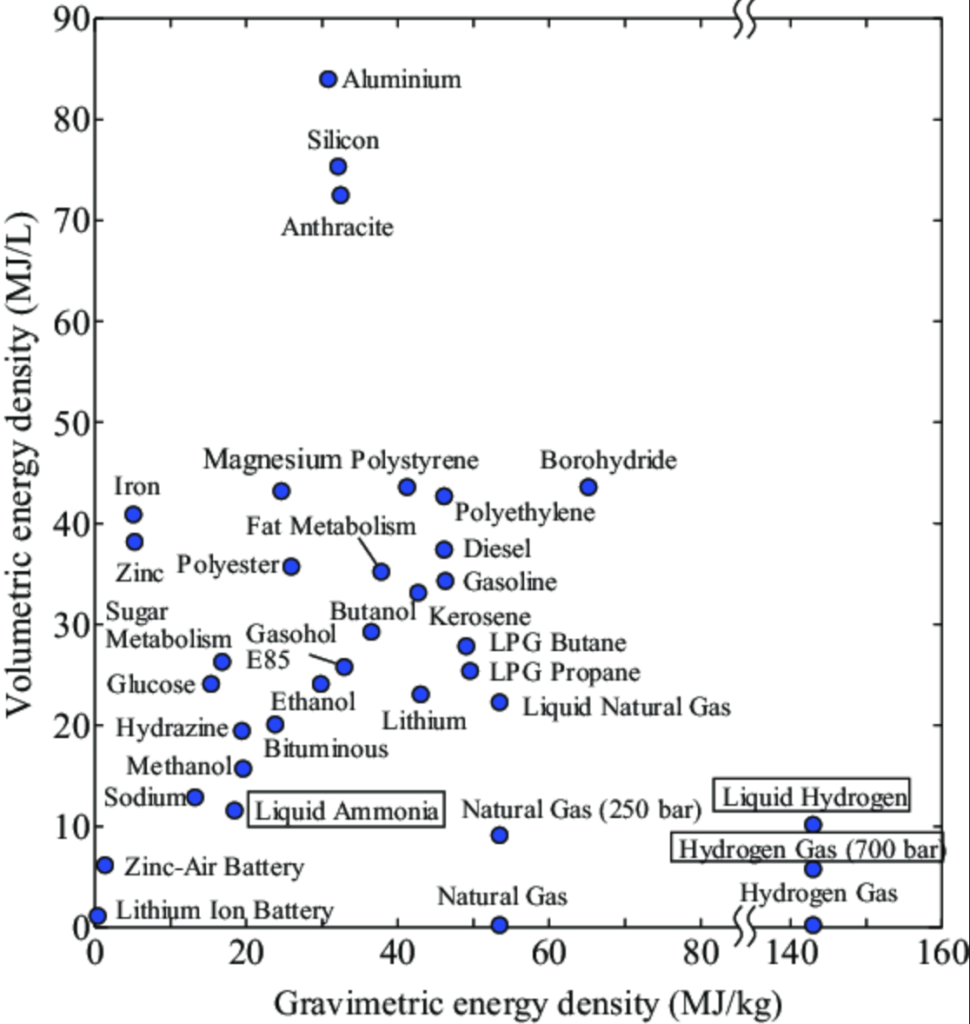

Compared to other candidate clean fuels and fossil fuels, liquid ammonia sits somewhere in the middle of the pack in terms of gravimetric and volumetric densities. It has both lower gravimetric and volumetric densities than gasoline and diesel as well as E85 gasohol. However, it trumps lithium-ion batteries in both and comfortably beats gaseous hydrogen (both 350 bar and 700 bar) in volumetric density. Furthermore, ammonia is liquid at ambient temperature, making it easier to store and transport than hydrogen.

The calorific value of ammonia is 22.5 MJ/kg or about half that of diesel. In a normal engine, in which the water vapor is not condensed, the calorific value of ammonia will be further less (about 20% less). Overall, ammonia is far less energy dense than gasoline and diesel. Ammonia is also more difficult to ignite than gasoline and diesel. It is unclear whether ammonia-powered cars can compete with traditional ICEVs or even EVs.

As one of the most produced and transported chemicals, the infrastructure already exists. Still, ammonia as a motor vehicle fuel would require a significant change to current infrastructures, both in ammonia production and fuel storage and transportation.

Ammonia is a toxic and corrosive compound used extensively in agriculture and pharmaceutical, which raises concerns about safe handling and distribution. While ammonia is stored similarly to propane, fueling stations that can safely and effectively store and distribute ammonia will have several technical challenges and expensive.

Although ammonia is easier to transport and distribute than hydrogen, leakage is still a challenge that needs to be overcome. When released to the environment, though, it becomes a toxic gas. Liquid anhydrous ammonia expands ~850 times when released to ambient air and can form large vapor clouds.

Furthermore, ammonia engines release a significant amount of nitrogen into the atmosphere if they don’t maintain sufficient levels of high compression or boost. This means an improperly tuned or misfiring ammonia motor could potentially have devastating effects on health and the atmosphere.

Do ammonia-powered cars and trucks represent a new paradigm or just another new fad? Perhaps only time will tell.

]]>

**Note: This is part 2 of the DOE H2 Hubs series

The previous post looked at the feedstock of the 7 winning H2 Hubs. This time, we will look at the use cases proposed by these hubs. Collectively, these hubs are expected to produce a collective three million metric tons of hydrogen annually—30% of DOE’s 10 million metric tons/year goal by 2030.

Hydrogen: Jack of All Trades, Master of None?

Hydrogen is the Swiss-Army Knife of energy, able to do many things across various greenhouse gas emitting sectors. But, just as you won’t use a Swiss-Army Knife for all possible purposes, you also won’t use hydrogen for everything you could possibly do with it. (Michael Liebreich has a pretty good analogy in his old Hydrogen Ladder post.) As much hype as hydrogen is receiving in the cleantech space, the reality is that it will have to be competitive compared to incumbent energy sources. Clean hydrogen will need to be cheaper, better, more scalable, safer, more convenient than other solutions in order to win its way into the global economy.

In other words, if clean hydrogen is to be an integral part of the clean economy, the hubs will need to successfully demonstrated hydrogen’s role in various end-uses. And that’s why we are talking about the proposed use cases. But right now, clean hydrogen is a jack of all trade and a master of none.

DOE’s End-Use Diversity Focus

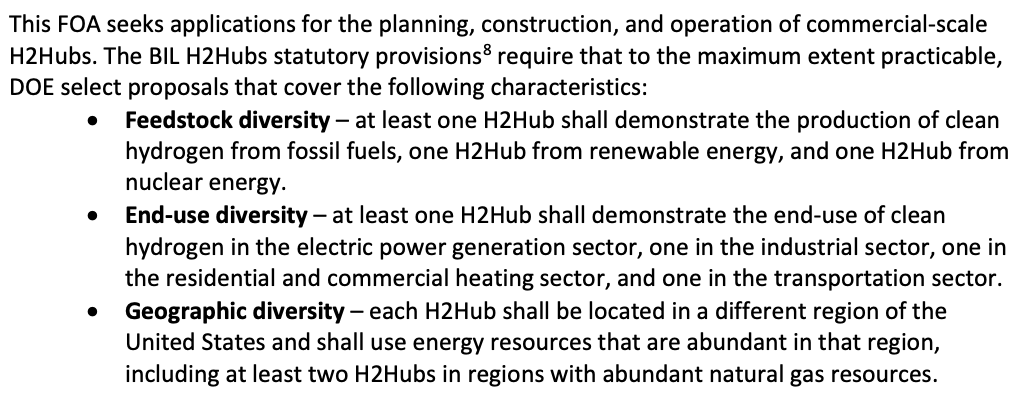

The Bipartisan Infrastructure Law (IIJA) required four end-use sectors to be included in the hubs: industry, transportation, power, and residential and commercial heating. Furthermore, the DOE funding opportunity announcement (FOA) was specifically looking for end-use diversity.

Frankly, the explicit inclusion of residential and commercial heating in the FOA is strange. For space heating in buildings, heat pumps are better and more efficient than hydrogen. Using renewable energy like wind to generate hydrogen and then using hydrogen for heat has a system efficiency of ~50%, compared to over 100% for heat pumps.

Another strange decision from the FOA is that DOE doesn’t seem to differentiate between use cases within a sector. For example, within the transportation sector, while hydrogen can be an excellent fuel candidate for aviation (IPCC category 1A3a) and shipping (IPCC category 1A3d), it is a poor choice for on-road light-duty vehicles (IPCC categories 1A3bi and 1A3bii).

Examining the Use Case Diversity of the 7 H2 Hubs

Here is a summary of the proposed end-uses of the 7 winning hubs:

At first glance, the selected hubs do appear to have a diverse proposed use cases collectively, spanning the transportation, industry, agriculture, and the buildings sectors as well as power generation. As expected, transportation and industry have the most sub-sectors and activities listed as proposed end-uses.

Heavy-duty transportation (trucking, buses) lead the way, with 5 hubs proposing it as an end-use, followed by power generation and aviation with 3 hubs.

But is the pursuit of diverse end uses at the expense of optimal allocation of use cases?

It is complicated to say. On one hand, hydrogen may be great for application such as hydrogenation and hydrocracking (a source of diesel and jet fuels), but these applications are rather niche and make up only a sliver of total GHG emissions. On the other hand, hydrogen’s competitiveness varies greatly even within a sub-sector. For example, international shipping, river cruises, and local ferries all fall under the shipping, a transportation sub-sector. Hydrogen ranges from having great potential for decarbonizing international shipping to being uncompetitive for local ferries (where battery-powered ferries may be more suited).

Interestingly, Heartland is the only winning hub that has space heating as a proposed end use while also being the only one without any transportation end-uses. Meanwhile, ARCHES is the only one that has public transportation as a proposed use case. But the problem is, public transportation just doesn’t need hydrogen in most cases. Shuttles and buses don’t travel long distances in a given day, stops frequently to pick up and drop off passengers, have predictable routes, and have depots to return to at the end of every drive shift. Their drive cycles and duty cycles favor battery-powered versions over hydrogen fuel-cell ones. Trains? Probably easier and more economically feasible to electrify the tracks instead.

What about trucks? The majority of the trucks on the road are regional. They might not cover enough miles for hydrogen to make sense. Regional trucks also tend to have a base to return to at the end of shift like buses. That leaves long-distance trucks, which make up a fraction of the trucking fleet but travel a disproportionately large share of vehicle miles. Hydrogen fuel cell could make sense, but current FCEV trucks are multiple times more expensive than diesel-powered trucks or even BEV trucks.

Finally, use cases where hydrogen could really make sense (e.g., fertilizer, ammonia, methanol, and steel production) aren’t popular: each has only 1-2 hubs proposing as end uses. And of these use cases, only fertilizer has no alternative to hydrogen; the rest can be produced using either biofuels or electricity or powered by batteries.

Conclusion

Did DOE miss the mark in the selection process with respect to use cases? Maybe, maybe not. Sure, there are better or worse use cases for hydrogen. Some of these hubs might not even make it to later stages of funding or live up to their promises. But for now, we can expect clean hydrogen supply to remain limited for many years to come. DOE should focus its investments on use cases where hydrogen is irreplaceable instead of making many bets across several use cases.

]]>

All Aboard the Hydrogen Hubs Hype Train

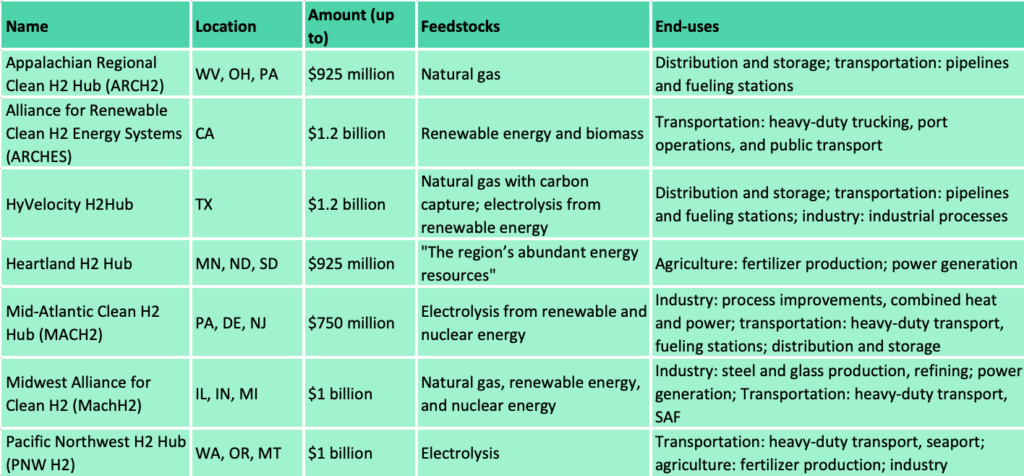

The U.S. Department of Energy (DOE) on Friday announced its selection of 7 much anticipated regional hydrogen hubs (H2Hubs), totalling $7 billion in awards. These hubs are located in various parts of the U.S.—the Appalachia, California, the Gulf Coast, the Northern Great Plains, the Mid-Atlantic, the Midwest, and the Pacific Northwest. Collectively, these hubs are expected to produce a collective three million metric tons of hydrogen annually—30% of DOE’s 10 million metric tons/year goal by 2030.

The following table summarizes these 7 H2Hubs:

Hydrogen can be produced from diverse domestic resources and used across sectors. Production can be centralized or decentralized, grid-connected or off-grid, offering scalability, versatility, and regionality. Hydrogen can be produced from several technology pathways, feedstocks, and have several potential end-uses. It is no wonder that the Biden administration is all-in on the hydrogen hype train.

Recall that the funding opportunity announcement (DE-FOA-0002779) has three selection criteria focused on diversity: feedstock diversity, end-use diversity, and geographic diversity (see excerpt above). At first glance, the selected H2Hubs have covered these three fronts very well. But is that the whole story?

Hydrogen Hubs: A Cash Grab for Big Oil and Gas?

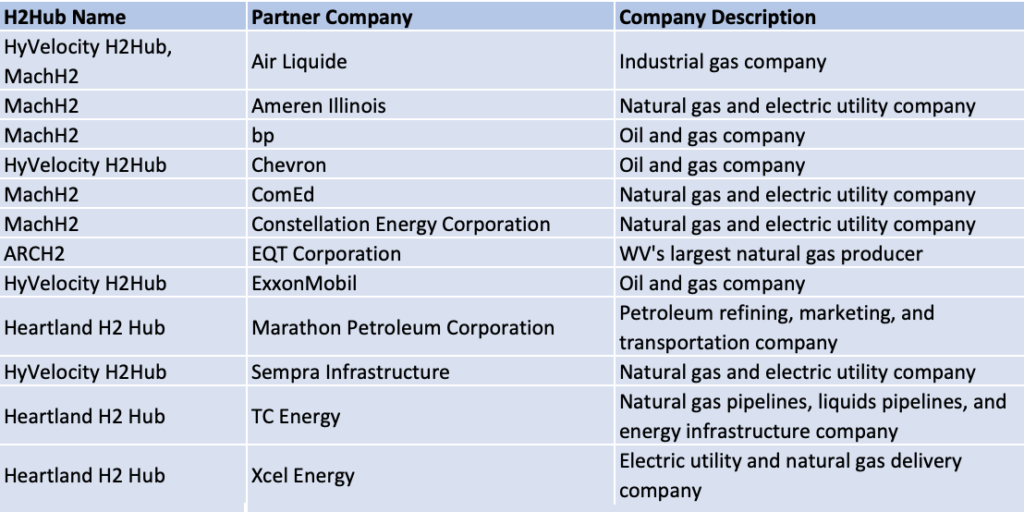

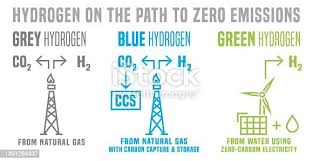

4 out of 7 H2Hubs (ARCH2, HyVelocity H2Hub, Heartland, and MachH2) will produce hydrogen using natural gas, a fossil fuel. This means over half of the H2 hubs will produce so-called blue hydrogen (using fossil fuels with carbon capture and storage). Right now, blue hydrogen is cheaper but dirtier than hydrogen produced from electrolysis from renewable energy and nuclear energy. Of these hubs, ARCH2 will produce hydrogen exclusively from fossil fuel.

Indeed, industry partners backing these 4 hubs include major oil and gas companies. See the table below.

Unfortunately, even the hubs that plan to produce hydrogen using electricity generated from renewable energy and/or nuclear energy aren’t blameless either. In a previous post, I wrote that a lot of renewable energy are waiting to be interconnected due to grid backlog. the grid is woefully outdated and there are not enough transmission lines to support the transition from a fossil fuel-based electric system to a decarbonized energy grid. This means the H2Hubs that plan to produce hydrogen from electrolysis should not divert clean energy from the grid. Otherwise emissions from electricity generation would increase.

Except for ARCH2, these hubs plan to use several methods for hydrogen production, but the exact mix may change depending on which projects make it through the DOE negotiations process. Although the Biden administration has emphasized that roughly two-thirds of the $7 billion pot is associated with the production of hydrogen from renewable energy, it’s too early to tell what the final result would look like (these hub demonstrations will run until around 2032, providing that they meet the milestones set by DOE.)

The next post will look at the end-uses proposed by these hubs.

]]>

In this NOI, DOE is seeking public input on the design of a demand-side support mechanism for the regional clean hydrogen hubs program. (In an earlier announcement, DOE plans to spend up to $7 billion to support 6 to 10 clean hydrogen hubs throughout the U.S.)

There is nothing wrong with wanting to provide additional support (Section 45V hydrogen tax credit, anyone?) to ramp up the market for clean hydrogen. The main issue is, the questions that DOE is asking are fundamentally economic questions, but DOE’s main bread and butter is early stage research and development.

And it shows in the NOI. The NOI has several uncertainties that make the economic feasibility of such support mechanism questionable. For example, the NOI did not specify who would be receiving the support (customers? end users? the hubs?) Depending on who receive the support, $1 billion ranges from very little to a mere drop in the bucket.

How little? In DOE’s recently published National Clean Hydrogen Strategy & Roadmap, the intermediate goal is to produce 10 MMT per year by 2030. That’s right: 10 billion kg by 2030. So that $1 billion amounts to 10 cents per kg… for a year. (For reference, DOE has a goal of reducing the cost of clean hydrogen to $1/kg in a decade [“1 1 1”]. Green hydrogen costs ~$5/kg today.)

Another important consideration is these hubs are silo, which means they face little to no competition from each other presumably. The hubs will be a mix of blue hydrogen (using fossil fuels with carbon capture and storage), green hydrogen (electrolysis from renewable energy), or pink hydrogen (using nuclear energy). It is not clear how DOE will handle the competitive process. Right now, blue hydrogen is cheaper but dirtier than green and pink hydrogen; such a support mechanism might end up blocking the market entry of green/pink hydrogen.

Speaking of silo hubs, the initial market will likely be a captive market. How does a captive market affect demand stimulus? It is possible that it would end up limiting competition (which means a lower level of clean hydrogen on the market than intended.)

Finally, the NOI asked about the effectiveness of “pay-for-difference contracts“, which I will assume to be synonymous to “contract-for-difference” or CfD. A CfD is a private law contract between a vendor and a customer at an agreed fixed price for a number of years. (Disclaimer: I am not a lawyer and know nothing about financial, commodity, or energy laws.) The energy generation market in the U.K. is perhaps the most well-known example of CfD application. While CfD is the British government’s main mechanism for supporting low-carbon electricity generation, it is banned in the U.S. (see Security and Exchange Commission v. 1Pool Ltd.) It isn’t clear in the NOI whether DOE has considered potential legal issues that could arise from implementing a CfD scheme (where do you draw the line between financial instruments and commodities? Is energy in an energy market considered a commodity? What about commodity derivatives?)

Ultimately, if DOE is concerned that there might not be enough demand or offtakes or hydrogen hubs’ competitiveness, perhaps it might be more effective to help the hubs directly?

]]>