In this NOI, DOE is seeking public input on the design of a demand-side support mechanism for the regional clean hydrogen hubs program. (In an earlier announcement, DOE plans to spend up to $7 billion to support 6 to 10 clean hydrogen hubs throughout the U.S.)

There is nothing wrong with wanting to provide additional support (Section 45V hydrogen tax credit, anyone?) to ramp up the market for clean hydrogen. The main issue is, the questions that DOE is asking are fundamentally economic questions, but DOE’s main bread and butter is early stage research and development.

And it shows in the NOI. The NOI has several uncertainties that make the economic feasibility of such support mechanism questionable. For example, the NOI did not specify who would be receiving the support (customers? end users? the hubs?) Depending on who receive the support, $1 billion ranges from very little to a mere drop in the bucket.

How little? In DOE’s recently published National Clean Hydrogen Strategy & Roadmap, the intermediate goal is to produce 10 MMT per year by 2030. That’s right: 10 billion kg by 2030. So that $1 billion amounts to 10 cents per kg… for a year. (For reference, DOE has a goal of reducing the cost of clean hydrogen to $1/kg in a decade [“1 1 1”]. Green hydrogen costs ~$5/kg today.)

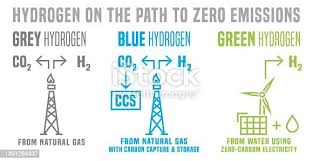

Another important consideration is these hubs are silo, which means they face little to no competition from each other presumably. The hubs will be a mix of blue hydrogen (using fossil fuels with carbon capture and storage), green hydrogen (electrolysis from renewable energy), or pink hydrogen (using nuclear energy). It is not clear how DOE will handle the competitive process. Right now, blue hydrogen is cheaper but dirtier than green and pink hydrogen; such a support mechanism might end up blocking the market entry of green/pink hydrogen.

Speaking of silo hubs, the initial market will likely be a captive market. How does a captive market affect demand stimulus? It is possible that it would end up limiting competition (which means a lower level of clean hydrogen on the market than intended.)

Finally, the NOI asked about the effectiveness of “pay-for-difference contracts“, which I will assume to be synonymous to “contract-for-difference” or CfD. A CfD is a private law contract between a vendor and a customer at an agreed fixed price for a number of years. (Disclaimer: I am not a lawyer and know nothing about financial, commodity, or energy laws.) The energy generation market in the U.K. is perhaps the most well-known example of CfD application. While CfD is the British government’s main mechanism for supporting low-carbon electricity generation, it is banned in the U.S. (see Security and Exchange Commission v. 1Pool Ltd.) It isn’t clear in the NOI whether DOE has considered potential legal issues that could arise from implementing a CfD scheme (where do you draw the line between financial instruments and commodities? Is energy in an energy market considered a commodity? What about commodity derivatives?)

Ultimately, if DOE is concerned that there might not be enough demand or offtakes or hydrogen hubs’ competitiveness, perhaps it might be more effective to help the hubs directly?

]]>